The Archegos family office debacle is symptomatic of a deeper problem for public investors in equity markets. Regulators are asleep to what anonymous traders are doing in dark equity markets and the risk they pose to investors.

Archegos used a financial instrument to obscure its holdings from regulators called total return swaps with six major banks. The stocks the family office held were in the name of the banks, not their name. Thus, total return swaps hid from regulators disclosure information that funds, brokers, and significant investors must report. Archegos even used the same stock collateral with all six banks. Using the same collateral is a violation of bank financing agreements. Yet, the banks somehow did not know how leveraged Archegos was until their stocks lost value below margin limits. Two banks got out quickly while Credit Suisse lost $5.5B and four others lost billions in forced stock sales. During the debacle, six banks sold $30B in stocks over a few days, sinking individual stock prices, remaining depressed.

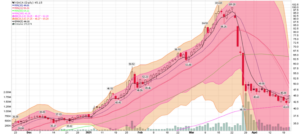

Stocks like VIACOM CBS declined 60% after the quick Archegos selloff in late March and remain depressed.

Source: P. Hill – Stockcharts.com – 4/21/21

Investors lost millions of dollars in VIACA stock alone and millions in other stocks like the Discovery Channel, a major Archegos investment.

There are 10,000 family office investment entities managing $6T in assets where regulators have little visibility into their leverage and risks. In addition, other principal family offices have significant positions in stocks that could have a substantial impact on equity prices for all investors. Therefore, the same disclosure and margin rules that apply to hedge funds, mutual funds, and investment banks should apply to family offices.

An investor advocacy group, Americans for Financial Reform, in a letter to the Securities and Exchange Commission, called for more disclosure by family offices:

“There is no reason why large investors whose decisions can significantly impact other investors and companies should be able to avoid the same scrutiny other investors face simply because of how they choose to structure their trade or their investment firm,” the group noted in a letter to the SEC. “

How many more Archegos family office risk-taking entities are in the markets today? No one knows the answer. Investors incurred massive losses in ViacomCBS and Discovery stocks. Investors must absorb millions of dollars in losses due to a massive risk by a single-family office.

The SEC needs to focus on protecting small investors from market manipulation of major players like family offices to restore trust in the stock market system.

In addition, regulators should review the way ‘dark exchanges’ have distorted market prices. Over 40% and sometimes up to 50% of market volume goes to off public exchange pools. These dark markets operate for market players like pension funds, investment banks, sovereign funds, and other entities looking to hide their trades. Brokers like Interactive Brokers offer Dark Ice, Hidden, and other stock buy and sell actions to keep trading actions anonymous. Thus, reducing the visibility of their trades making them hidden from other traders. This opaque price discovery system leads to extreme risk-taking and unregulated price manipulation.

In the U.S., dark pool hedge funds lost billions when social media day traders went after hedge fund short positions. GME Stop prices were distorted when day traders ganged up on short-sellers by buying the stock to drive up the price and force short-sellers out. The extreme price swings caused brokers to post billions to settle stock trading accounts when stocks were purchased on margin.

Other countries do not allow off public exchange trading. For example, Canada does not allow zero commission pay for flow stock transactions to dark pool exchanges. Canadian regulators set the policy to make stock markets more transparent and less prone to manipulation. Since 2018 the European Union has largely banned dark pool trading for transparency reasons as well. Britain, is now financially severed from the EU. The country’s financial leaders are expressing interest in opening up dark pool trading to generate business lost to Frankfurt and Amsterdam. However, it’s still unclear if regulators in Britain will make a move to allow dark pool exchanges.

The point is this: to build trust in price discovery for all investors; all stock transactions should be transparent. Major institutions should reduce the impact on prices by packaging their trades into smaller tranches. Only when investor participates at the same level of visibility will trust be restored in exact market pricing mechanisms. Plus, price manipulation will decline.